Let us do Nvidia Stock Q2 Report Analysis based on their Q2 2023 earnings released recently. The stock price action has been very volatile. In November 2021, it was worth $334 per share before plummeting by around 66% to $112. Since then, the stock has surged over 180% and further increased by 24% after the earnings release.

Upon initially reviewing the earnings report, it didn’t seem impressive; however, strong guidance led to continued rallying and an additional 24% increase in value today. This rapid growth is remarkable as Nvidia’s valuation jumped from $754 billion to approximately $940 billion overnight – almost a $200 billion increase based on their latest earnings announcement.

Nvidia’s Mixed Results: Data Center and Auto Growth

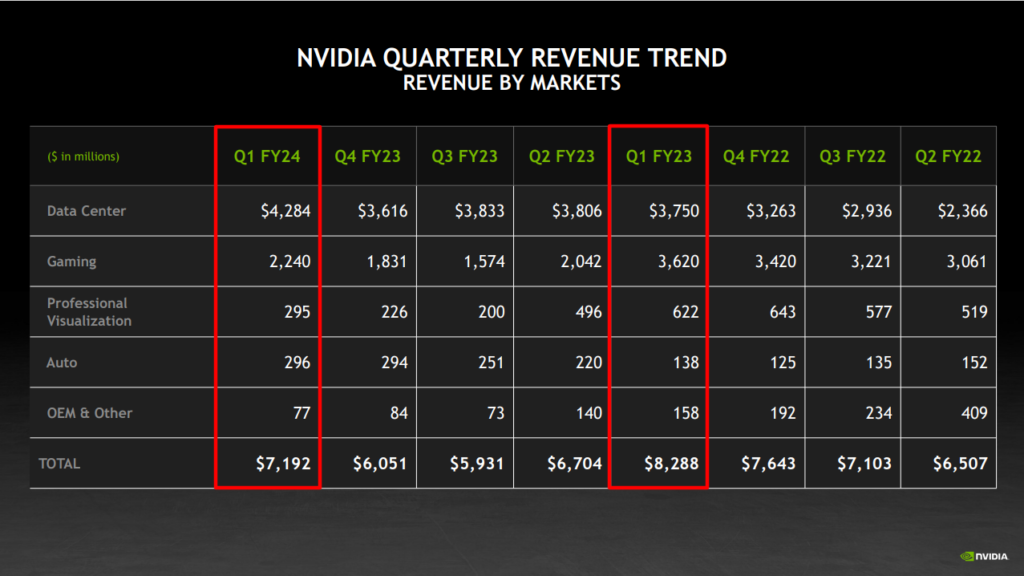

In Nvidia’s latest report announced recently, we can examine their different revenue segments: data center, gaming, professional visualization, auto, OEM, and total. The company generated about $7.2 billion in revenue for this quarter compared to $8.3 billion during the same period last year – a 13% decline.

Upon first glance, the report may not seem impressive; yet some aspects caught investors’ attention. Notably, data center revenue increased by roughly $500 million while auto revenue doubled with an additional $150 million year over year. These two sectors are experiencing growth within Nvidia’s business.

On the other hand, gaming decreased by approximately $1.4 billion; professional visualization fell 50%, losing around $300 million; and OEM dropped 50%. Consequently, it is clear that data center and auto revenues are driving excitement in this report as they stand out amidst declining figures from other segments of Nvidia’s business.

Nvidia’s Data Center Growth and AI Adoption

Notably, there is a record data center revenue of $4.28 billion, indicating positive growth. The long-term potential for this business sector remains strong due to increasing AI adoption and businesses expanding their cloud and data infrastructure.

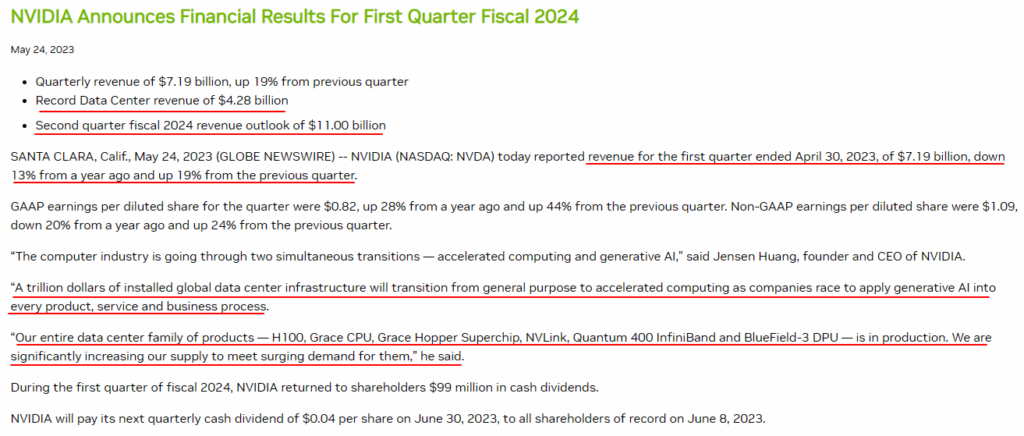

The second quarter fiscal 2024 revenue outlook for $11 billion has generated excitement, as it indicates a 50% growth from the previous quarter’s $7.2 billion revenue. This unexpected increase in revenue is driving the stock to all-time highs and raises questions about Nvidia’s short-term business prospects.

There are concerns that this surge in revenue may be due to the current hype surrounding artificial intelligence (AI). While AI will undoubtedly have long-lasting impacts, its current prominence could be compared to the electric vehicle bubble of 2020-2021. During that time, any company associated with electric vehicles saw massive increases in their stocks before eventually declining by up to 90%.

Revenue has decreased by 13% year over year but increased by 19% quarter over quarter. Nvidia predicts a significant shift in global data center infrastructure, as companies increasingly adopt generative AI for various applications. This transition is expected to lead to a $1 trillion investment in upgrading data centers.

Nvidia’s new technology aims to modernize these facilities, and they currently offer the best product in the market. Though no specific time frame is provided, this outlook aligns with Brookfield’s predictions as well.

The entire range of Nvidia’s data center products is now in production, and due to high demand, they are working on increasing supply significantly.

Nvidia’s Balance Sheet and Financial Stability

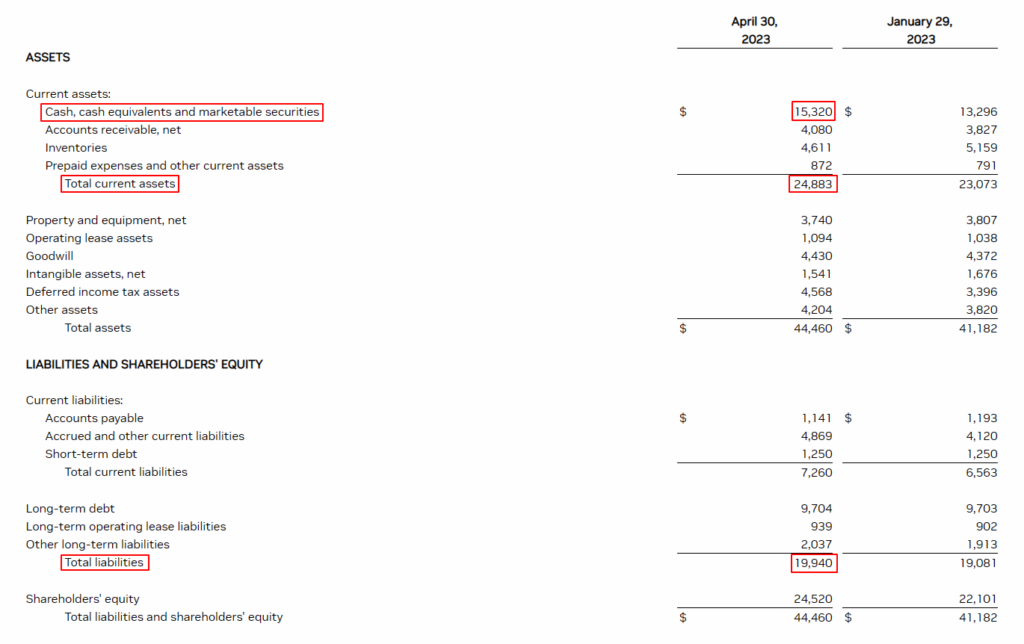

Now let’s examine Nvidia’s balance sheet, which is crucial when considering a new investment to assess the company’s financial stability. Nvidia holds an impressive $15.3 billion in cash and cash equivalents, contributing to their total current assets of around $25 billion.

Interestingly, their total liabilities amount to approximately $20 billion, meaning that Nvidia almost has enough cash on hand to cover all its liabilities. This indicates a strong financial position for the company. Furthermore, with their current assets at $25 billion, they could potentially eliminate all debt within the next year if desired. Although it may not be necessary or advisable for them to do so, this option highlights Nvidia’s solid financial standing as a business.

Nvidia’s Boosted Cash Flow and Reduced CapEx

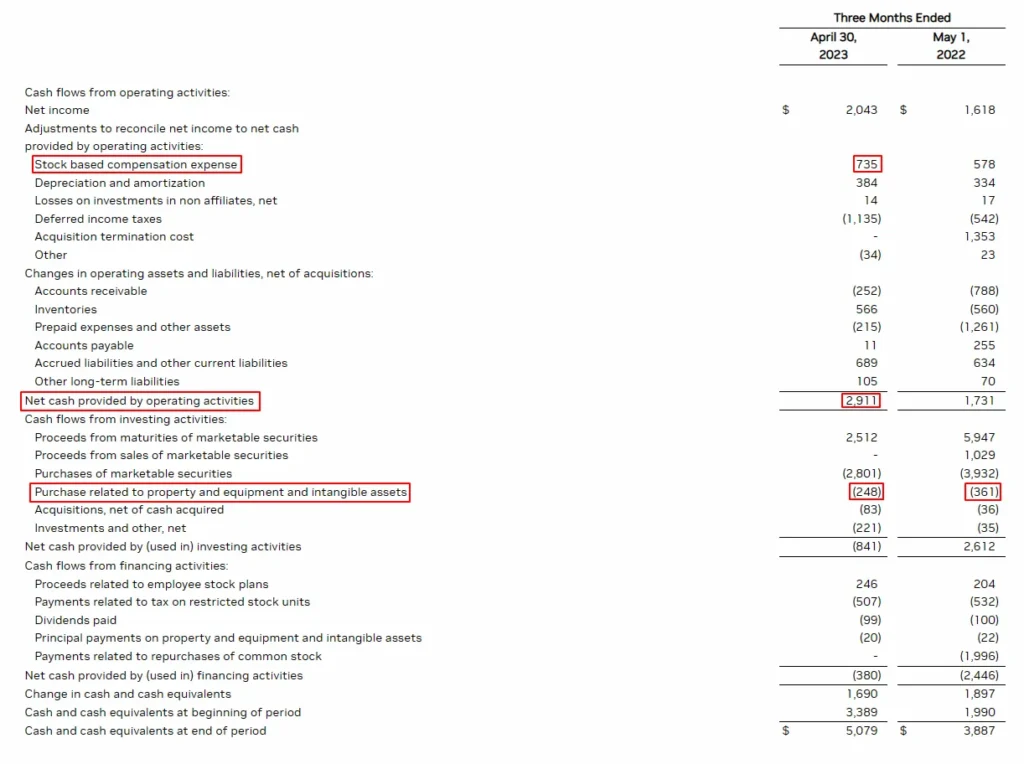

The cash flow statement highlights a strong quarter for Nvidia. Despite a 13% decrease in revenue year over year, the company’s operating cash flow nearly doubled, reaching $2.9 billion – an impressive increase of 70-80%. This growth is accompanied by a decrease in capital expenditures (CapEx), which dropped to $248 million from last year’s $361 million.

Nvidia has managed to significantly boost its operating cash flow while reducing CapEx spending by around 30%. This indicates that the company is efficiently generating free cash flow; CapEx accounts for less than 10% of the operating cash flow. In fact, Nvidia generated $5.1 billion in free cash flow over the past 12 months.

The solid financial performance supports the hype surrounding this fundamentally sound business. As one of the best computing companies and a leader in data centers and accelerated computing technology, Nvidia also boasts an attractive long-term growth prospect and excellent balance sheet.

Examining the company’s income statement, we see a downward trend in revenue. However, with next quarter’s guidance, it is expected to reach all-time highs. Operating cash flow has been declining for approximately 15 months or five quarters but is now beginning to increase as the company refocuses on efficiency. Despite this improvement, the business still isn’t generating record high cash flow and currently stands at 5.1 billion in free cash flow.

Nvidia’s Valuation: Examining Price-to-Free Cash Flow

Examining Nvidia’s price-to-free cash flow raises concerns about its current valuation. Although Nvidia is a fundamentally strong business, it trades at an incredibly high price-to-free cash flow of around 200. This situation reminds us of the electric vehicle bubble in 2020 and 2021 when we saw similar price ratios.

While Nvidia is undoubtedly a great company, the market seems to have already priced in its excellence and an excessive amount of future growth. Main reservation with investing in Nvidia lies in its potentially overinflated value. To put this into perspective, such a valuation may not be justified.

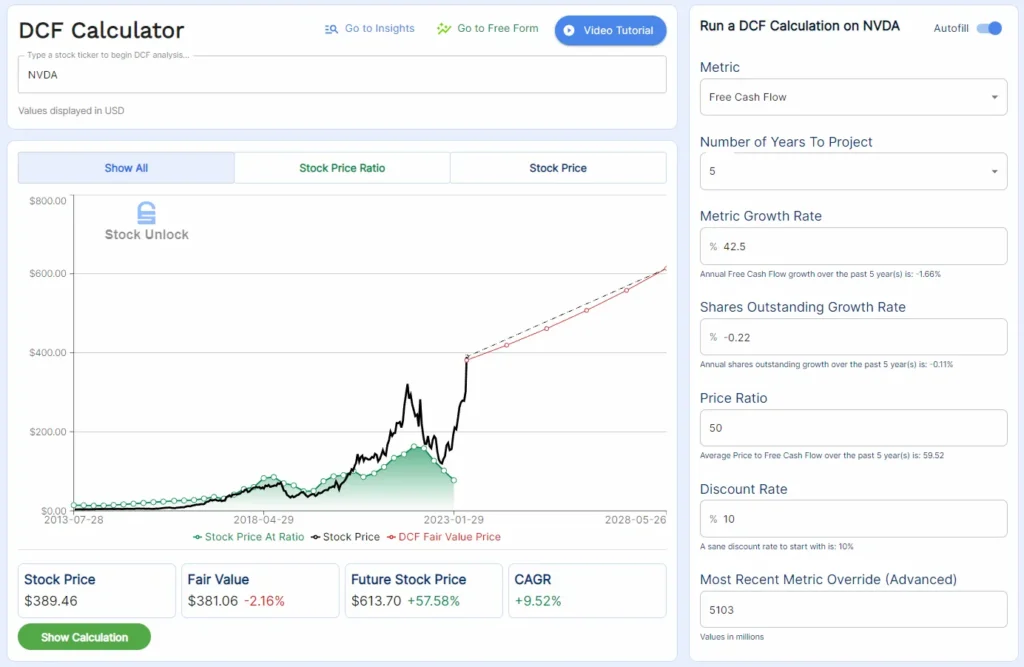

A reverse DCF calculation to determine the market’s current expectations for Nvidia’s stock would suggest whether the stock is overvalued or undervalued.

Projecting Nvidia’s free cash flow over the next five years (until 2028) and assuming a growth rate of 42.5% with no annual share buybacks and a price-to-free-cash-flow ratio of 50, the stock’s fair value today can be calculated. If these metrics are met, the stock should achieve a compounded annual growth rate (CAGR) of 10%, similar to historical S&P 500 returns.

Nvidia’s growth of free cash flow at a CAGR of 42.5% while maintaining an expensive price-to-free-cash-flow ratio in five years’ time seems overly optimistic; achieving such high growth rates is challenging.

If Nvidia fails to meet these ambitious targets, it may not outperform historical market returns as currently priced into its valuation. To exceed S&P 500 returns moving forward, it would need even better performance than our calculated metrics suggest.

There is significant future growth and performance already factored into Nvidia’s current valuation; this presents risks if the company falls short of these lofty expectations and could result in subpar investment returns or potential depreciation.

In summary, to achieve the 42.5% free cash flow growth rate projected for Nvidia over the next five years, the company would need to generate about $30 billion in free cash flow by 2028. Currently, it produces $5 billion annually, meaning it must increase its cash flow sixfold within this period. This expectation seems overly optimistic and too expensive for investment. While Nvidia is an excellent business, its current valuation is too high to spark much interest.

One thought on “Nvidia Stock Q2 Report Analysis | Key Insights on the Soaring NVDA Stock”

Comments are closed.